Rock You Like a Hurricane

Corie and I first made the 15 hour trek down I-75 in 1996. Probably my most memorable visit was the drive when the twins were 9 months. We visited a rest stop in northern Florida and fed them as they sat in their car seats. I fell in love with Venice, FL as a result of these trips. Our three daughters enjoyed many spring breaks on the beach with grandma and great grandma. And the bike rides around the “island” with my father-in-law were great relief from the corporate grind. Fast forward to February 2022. Corie and I pulled the trigger and bought a house in Venice. It took only 7 months for us to realize the downside of my dream purchase and the importance of insurance.

Corie and I talked for a long time about buying a house in Florida. It’s not for everyone, but I’ve always enjoyed the warm weather to offset the 5 months of cold and gray in Cincinnati. And the town of Venice, designed by landscape architect John Nolen who also designed Mariemont, OH, is a unique place. It has a cool “island” with tennis courts, a boulevard with ice cream and shops, a labyrinth of bikeable side streets and the beach.

Financial advisor Dave warned me about the ongoing expenses of owning two homes. Financial advisor Brian was more direct – “don’t buy it”. I respect these two more than just about anyone. And like any good client, I ignored both of them. As the purchase went through, I realized the challenge of buying insurance in Florida. After 20 years of exorbitant claims, mostly roof claims, the insurance industry is ready to cry “uncle”. I’ve had exactly zero homeowner’s claims in 27 years of policies, so the thought of a $3500 policy was abhorrent. We pushed forward and grudgingly paid.

Hurricane Ian hit Florida the last week in September. While the news focused on Naples, Fort Myers and Punta Gorda because of the direct hit, Venice was dealt a glancing blow. And by glancing, I mean 100+ MPH winds and 10” of rain. I got text reports from people in the area. First, I got an all clear based on a drive by. Then a picture with the fence strewn about. Finally, our neighbors came home and broke the real news – the top half of a neighbor’s 60’ pine tree had broken off. Mother Nature and her 120 MPH winds deposited it on our house. The tree destroyed the roof. Branches punctured through the ceiling. A bedroom, closet and bathroom need a major overhaul. As I type this, we are awaiting a response from the insurance company. The bottom line is, if a hurricane might come through, it behooves all of us to take precautions.

————————————————————————————————————————————————————-

The month of October has been good for the stock market. The S&P 500 is up about 8% for the month with the Dow up nearly 14%. Tech stocks are also up for the month at 4%. It’s always hard to draw big conclusions off one month. It’s looking increasingly likely that the midterms may usher in a Republican Senate and House. Historically, when the President is a Democrat and Congress is led by Republicans, markets do well. It’s also possible the market is sniffing out a pause to the interest rate hikes. After all, the Fed hasn’t raised rates this quickly since the early 80’s.

I think it’s more likely this is a pause in the bear market. Bull and bear markets tend to go through cycles. The S&P is still down 19% for the year and tech stocks (defined as the NASDAQ 100) are down 30%. Most recently, Facebook, Amazon and Google have all announced disappointing quarterly numbers. I expect more of these announcements in the coming months. The Fed continues to raise rates and has said it wants unemployment to go up and the economy to cool so that it can tamp down inflation.

On the consumer front, evidence says slowdown. I’ve included graphs of home sales in the past few newsletters. Today I’ll mention used cars. The chart below shows that used vehicle sales have dropped significantly, down about 17% from a year ago. There is a used car lot down the street from our office. They had zero cars a year ago. Today they have a dozen or so. And some of the cars have stickers that say “Make an offer”.

That said, the middle to upper end of the income curve continues to spend. Anecdotally I can say that Corie’s art business is still robust. Lots of new business and clients are tipping like never before.

We know a lot of you are nervous. You’ve told us. It’s never easy to watch account balances go in the negative direction. And our world has gotten increasingly confusing. The truth from our elected leaders and media is as gray as a December day in Cincinnati. Enter insurance.

Insurance takes many forms. You could hide in annuities. We don’t love annuities. Annuities are best for those who sell them. As Dave likes to remind me, the two biggest buildings on the Cincinnati skyline are insurance companies.

Many of you have large sums in “emergency funds”. That’s a form of insurance. We’ve raised cash in your accounts, another form of insurance. Recently, we tacitly admitted we weren’t happy with much of the bond market and bought Treasuries in many of your accounts. FDIC deposit insurance is often viewed as the holy grail. Well, Treasuries are even more safe. There is no $250,000 limit on Treasuries. And the FDIC insurance is provided by none other than the government. If the government were to default on its obligations, Treasuries, we’d have bigger worries. And short-term Treasuries are yielding around 4%, well into the range we generally like to get from bonds.

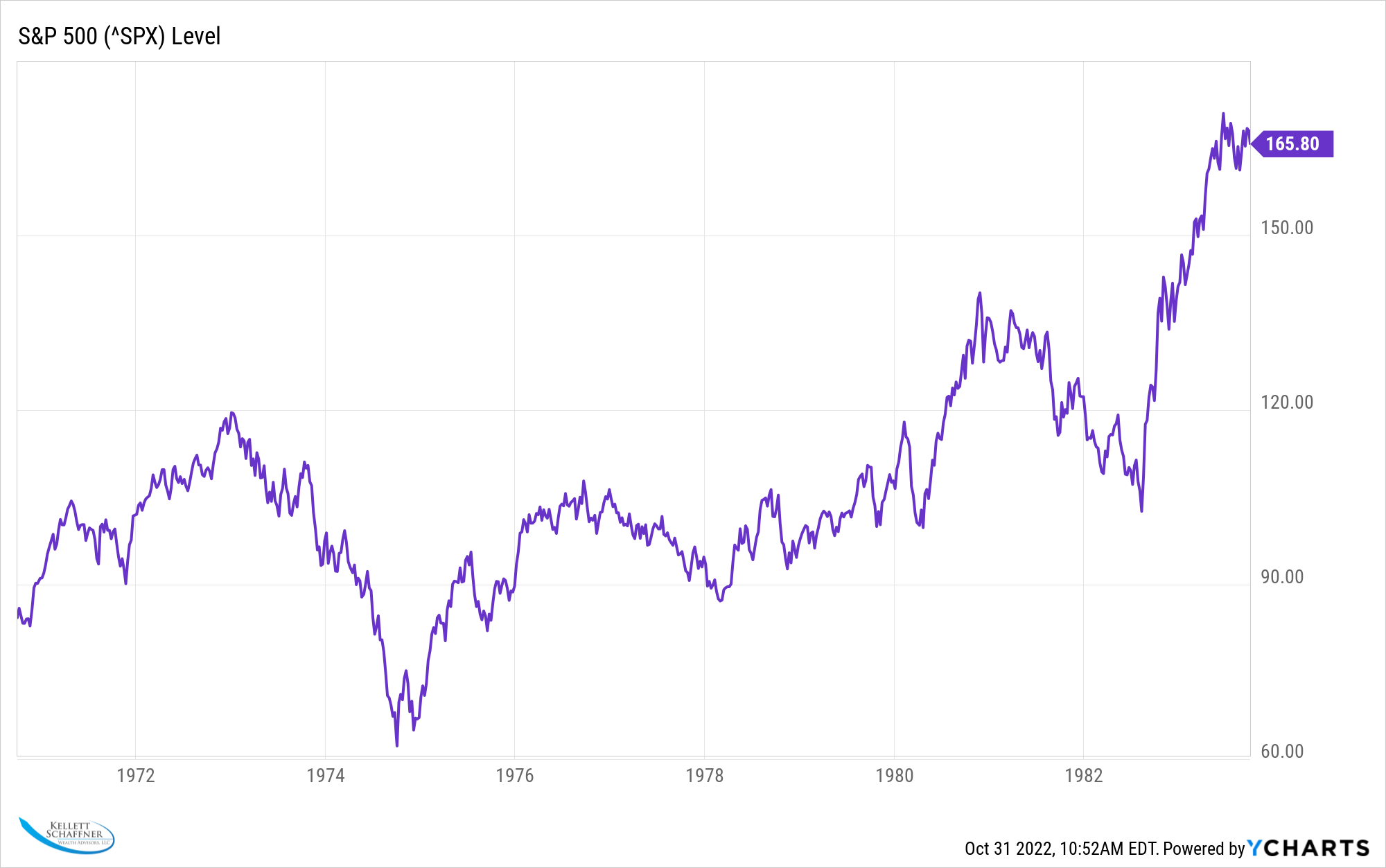

We continue to believe the markets will be choppy. Once the inflation genie is out of the bottle, it takes time to put it back in. As you can see below from the 70s, the US experienced three recessions (gray bars) and two interest rate hiking periods (orange line) to get inflation back down to 2ish%.

At the same time, it’s always worth keeping in mind that, while the 70s inflation was ugly, the S&P 500 still managed to go up from 86 to nearly 166, almost doubling.

So, rather than putting everything in cash, it’s usually better to trust the market will go up over time. We will be here to help you navigate your insurance options so that you aren’t rocked like a hurricane.

Jared

Brian Kellett, CFP brian@kellettschaffner.com. Phone 513-312-6067

Dave Bodnar, CFP david@kellettschaffner.com. Phone 513-258-6973

Jared Kline, CFP, EA jared@kellettschaffner.com. Phone 513-768-2238

Kellett Schaffner Wealth Advisors LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where Kellett Schaffner Wealth Advisors LLC and its representatives are properly licensed or exempt from licensure. This website is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Kellett Schaffner Wealth Advisors LLC unless a client service agreement is in place.

Government cheese statistics from Wikipedia. The story about Mr. Wilson is true to the best of my memory. YCharts are created by yours truly.